The insurance crisis spreading across the United States arrived at Richard D. Zimmel’s door this month in the form of a letter.

Zimmel, who lives in the increasingly fire-prone hills outside Silver City, New Mexico, had done everything right. He trimmed the trees away from his house and covered his yard in gravel to stop flames rushing in from the forest near his property. In case that buffer zone failed, he sheathed his house in fire-resistant stucco and topped it with a noncombustible steel roof.

None of it mattered. His insurance company, Homesite Insurance, dumped him. “Property is located in a brushfire or wildfire area that no longer meets Homesite’s minimum standard for wildfire risk,” the letter read. (Homesite did not respond to a request for comment.)

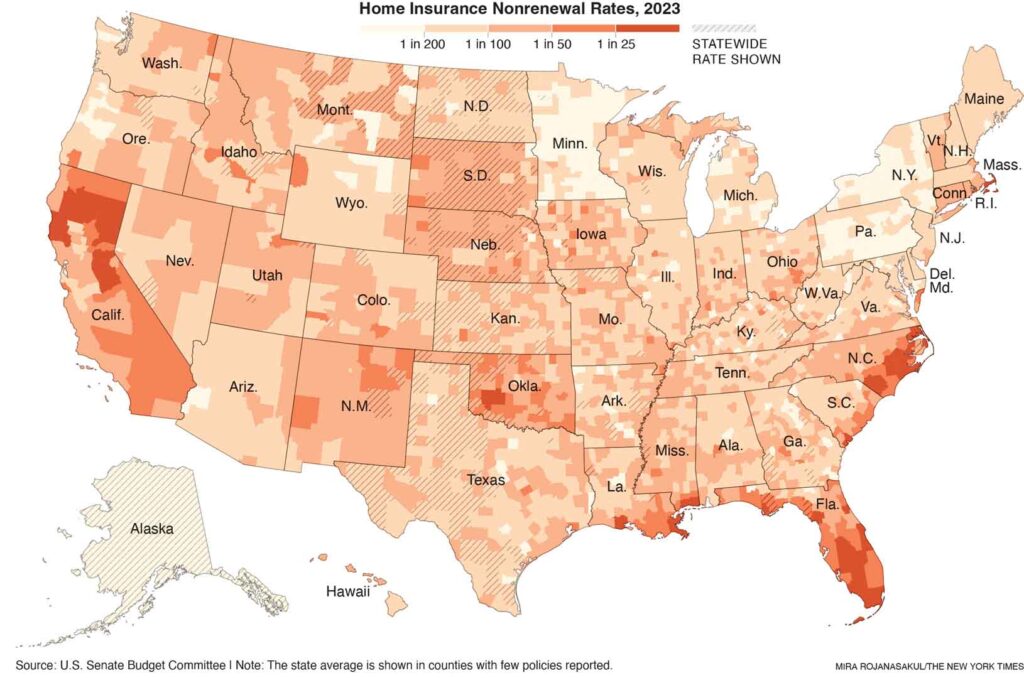

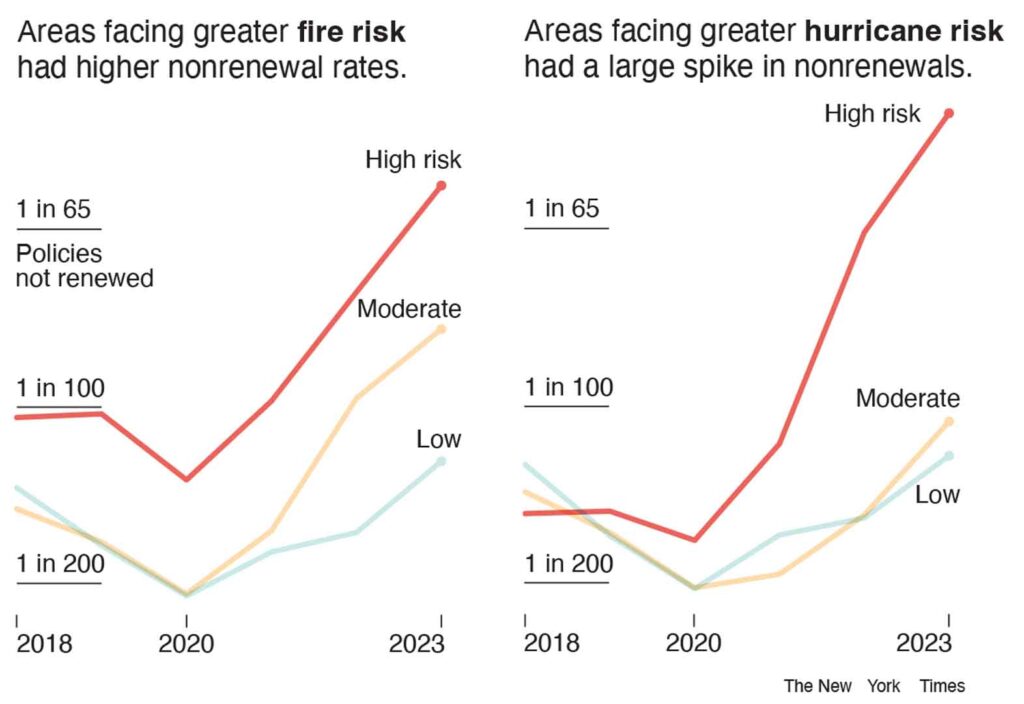

Zimmel has company. Since 2018, more than 1.9 million home insurance contracts nationwide have been dropped — “nonrenewed,” in the parlance of the industry. In more than 200 counties, the nonrenewal rate has tripled or more, according to the findings of a congressional investigation released Wednesday.

As a warming planet delivers more wildfires, hurricanes and other threats, America’s once reliably boring home insurance market has become the place where climate shocks collide with everyday life.

The consequences could be profound. Without insurance, you can’t get a mortgage; without a mortgage, most Americans can’t buy a home. Communities that are deemed too dangerous to insure face the risk of falling property values, which means less tax revenue for schools, police and other basic services. As insurers pull back, they can destabilize the communities left behind, making their decisions a predictor of the disruption to come.

Now, for the first time, the scale of that pullback is becoming public. Last fall, the Senate Budget Committee demanded the country’s largest insurance companies provide the number of nonrenewals by county and year. The result is a map that tracks the climate crisis in a new way.

The American Property Casualty Insurance Association, a trade group, said information about nonrenewals was “unsuitable for providing meaningful information about climate change impacts,” because the data doesn’t show why individual insurers made decisions. The group added that efforts to gather data from insurers “could have an anticompetitive effect on the market.”

Sen. Sheldon Whitehouse, D-R.I., the committee’s chair, said the new information was crucial. In an interview, he called the new data as good an indicator as any “for predicting the likelihood and timing of a significant, systemic economic crash,” as disruption in the insurance market spreads to property values.

The map of dropped policies shows how the crisis in the American home insurance market has spread beyond well-known problems in Florida and California. The jump in nonrenewals now extends along the Gulf Coast, through Alabama and Mississippi; up the Atlantic seaboard, through the Carolinas, Virginia and into southern New England; inland, to parts of the plains and Intermountain West; and even as far as Hawaii.

Silver City shows how the insurance crisis is a result of several factors over decades — and how hard it is to solve.

Founded as a mining town in the 1870s, the city of 10,000 nestles up against the foothills of the Gila National Forest, 3.3 million acres of alligator juniper, ponderosa pine and Gambel oak draped across softly sloping mountains.

That forest has also become a firetrap.

Since its designation as a national forest in 1924, the U.S. government sought to protect the land by stopping forest fires. That policy failed to take into account that fires clear out vegetation, according to Adam Mendonca, the U.S. Forest Service’s Washington deputy director of fire and aviation, who lives in Silver City. The result was the buildup of decades of additional trees and brush, which means wildfires, when they do happen, now burn larger and hotter.

That threat has been exacerbated by climate change, which has brought higher temperatures and drier conditions. Wildfires are now more likely to break out any time of year.

“We used to take our wildland gear home, put it into storage about September and then bring it back to the station in February,” said Milo Lambert, Silver City’s fire chief. “Now it doesn’t leave the trucks.”

Even as the threat of wildfires has grown, home construction has pushed farther into the forest. On a recent afternoon, Eric Casler, an assistant professor of natural sciences at Western New Mexico University, surveyed the neighborhoods that have grown north of the city limits.

“See all these scattered houses out here?” Casler said. If a wildfire started to burn through the area, “it’s going to be really hard for them to stop it.”

It’s not just where people build homes that puts them at risk, experts said, but how those homes are constructed. Outside city limits, Grant County has no zoning or wildfire building restrictions, and no inspection program to ensure that newly built homes are safe, according to Roger Groves, the fire chief for the county, which includes Silver City.

Taken together, those challenges have caused insurers to pull back, according to Susan Sumrall, an insurance agent in Silver City.

Across Grant County, 51 home insurance contracts were not renewed in 2018, based on the data provided to the committee. That’s about 1 in 100 policies. By last year, that number had doubled to 100 nonrenewals, even as the county’s total population shrank.

One of Sumrall’s clients who has lost her insurance is Charlene Rosati. Rosati and her husband had to spend months in Houston, where he was being treated for cancer. Her insurance company, State Farm, sent an inspector to check if the home was being properly maintained, Rosati said, and concluded it was not.

Rosati’s husband died in September last year. Soon after, State Farm told her it wouldn’t renew her coverage. The company did not respond to a request for comment.

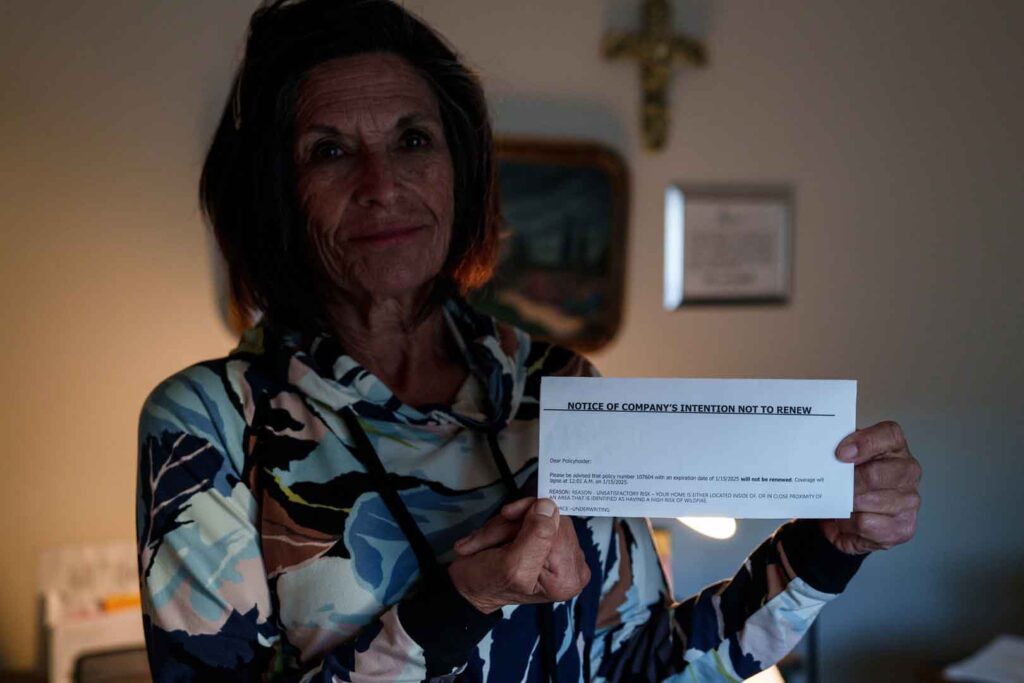

Many homes in and around Silver City are mobile or manufactured homes, which can offer less protection against fires than traditional site-built houses. Lorri Williams lives in a manufactured home in a valley just outside of Silver City. She, too, got a letter from her insurer, Standard Casualty Co., based in Texas.

“Reason — unsatisfactory risk,” the company wrote in block letters. “Your home is either located inside of or in close proximity of an area that is identified as having a high risk of wildfire.”

Standard Casualty did not respond to a request for comment.

People who lose insurance often don’t have great options. Williams’ broker, Chelsea Hotchkiss, tried getting her another insurer, with no luck. Hotchkiss suggested the state-run high-risk insurance program, which offers coverage to homeowners who can’t find it on the private market. But that program is more expensive and provides less coverage.

After Zimmel got his nonrenewal letter this month, he called State Farm, which declined to cover him. His insurance agent struck out with three more carriers, including Travelers. (State Farm and Travelers did not respond to requests for comment.) Finally, a smaller company agreed to insure his house, but his premiums jumped by one-third.

Zimmel’s bigger worry, he said, is how the struggle over insurance could affect his home’s value, which his real estate agent estimates at about $725,000.

“I just don’t know what’s going to happen to the town if this keeps happening,” said Zimmel’s agent, Shelley Scarborough.

Officials are trying to reduce wildfire risk. The county is looking at setting building standards to cut fire exposure, Groves said. State officials are also considering ways to get more homeowners to clear the vegetation from their property, possibly through a pilot project in nearby Lincoln County that would make those steps necessary to qualify for the state high-risk insurance pool.

And the U.S. Forest Service is trying to clear out decades’ worth of thick brush and other excess vegetation — what experts call “treating” the forest. That process is anything but simple.

In the parts of the forest nearest the city, workers have cut down smaller trees, low-hanging branches and scrub oak, then stacked them into piles to dry out. After a year or so, the piles are set on fire — ideally during the winter, to reduce the risk of the fire spreading.

After those two steps, the Forest Service can perform a prescribed burn — deliberately setting fire to a patch of the forest to further clear out the vegetation. To maintain that work, the process should typically be repeated every five to 10 years.

The Forest Service has been treating between 25,000 and 30,000 of the 3.3 million acres in the Gila forest each year, according to Mendonca. “It’s a constant struggle for the agency to try to address,” he said, citing a shortage of staffing, money and time.

The underlying challenges that are driving insurers from Silver City can be found across the country.

In parts of Wyoming, the growing risk of wildfire is similarly pushing insurers to drop customers. Teton County, which includes Jackson Hole, saw nonrenewal rates increase 1,394% since 2018. Jeff Rude, the state insurance commissioner, said the state was focused on educating homeowners about how to reduce the risk on their land, because tougher building standards are unpopular in Wyoming.

In California, which has some of the country’s most stringent building codes to address wildfire risk, insurers have nonetheless been fleeing. In some counties, nonrenewal rates have increased more than 500% since 2018. Officials announced this month that they would make it easier for insurers to raise rates, but in exchange, those insurers must agree to keep doing business in fire-prone areas.

In Hawaii, the nonrenewal rate tripled between 2018 and 2023, one of the highest increases in the country. The growing risk from wildfires and other threats has led to what Gov. Josh Green, a Democrat, has called a “condo insurance crisis.” In August, he signed an emergency proclamation, setting up a task force to search for solutions.

In coastal South Carolina, which now has some of the highest nonrenewal rates in the country, insurers have been going out of business, reducing their exposure or just leaving the area, said Jay Taylor, an insurance agent in Beaufort County, which includes Hilton Head, an area particularly exposed to sea-level rise, hurricanes and other climate threats.

Homeowners complain about the difficulty and cost of getting insurance, he said. But the desire to live by the ocean, despite the danger, remains the stronger force.

“They may cuss us out,” Taylor said. “But they never stop building.”

This article originally appeared in The New York Times.